Buying - How to decide how much to spend on your down payment

Buying a home is exciting. It’s also one of the most important financial decisions you’ll make. Choosing a mortgage to pay for your new home is just as important as choosing the right home.

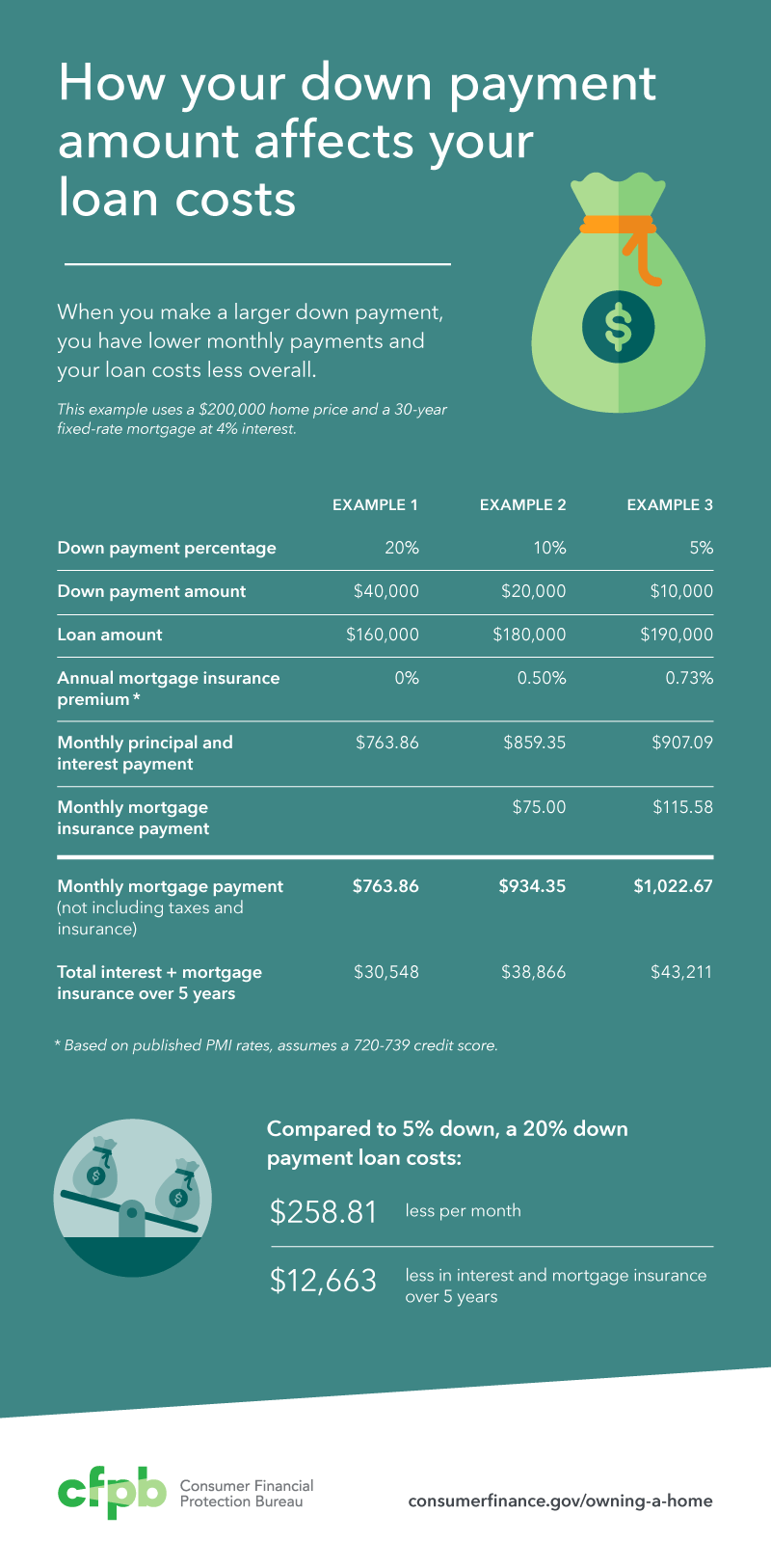

One of the toughest parts of buying a home for the first time is coming up with a down payment. You may have heard that in order to buy, you should have 20 percent of the total cost of the home saved up for the down payment. Actually, you can choose how much to put down based on what works best for your situation. Putting 20 percent down has a lot of benefits. However, saving enough money for a 20 percent down payment can be challenging, especially for first-time homebuyers. And, the money you put into your home is not available for other things, such as emergency expenses or other savings goals. There are a variety of mortgage options that allow you to make a down payment of less than 20 percent, but lower down payment loans are typically more expensive. In general, the less money you put down upfront, the more money you will pay in interest and fees over the life of the loan.

Key benefits of putting 20 percent down

You will have a smaller loan - which means lower monthly payments. With a larger down payment, you borrow less, so you have less to pay off. That means your monthly payments will be lower than with a smaller down payment.

You will have lower overall costs. When you borrow less, you’ll pay less interest on your loan. That’s because the interest is calculated using a lower loan amount. When you put down at least 20 percent, you also typically won’t have to pay for mortgage insurance. Mortgage insurance increases your monthly mortgage payment.

You start out with more equity, which protects you if the value of your home goes down. When you make a larger down payment, you have more of a cushion in case home prices decline. With a smaller down payment, you have a higher risk of owing more than your home is worth if market home prices decline, like they did between 2008 and 2012. If you owe more than your home is worth, it can be very hard to sell or refinance your home.

Mortgage Insurance

If you want to buy a home but can’t afford a 20 percent down payment, you will likely have to pay for mortgage insurance. Mortgage insurance protects the lender if you fall behind on your payments.

Where did the 20 percent number come from?

The “20 percent” threshold is based on guidelines set by Fannie Mae and Freddie Mac, government-sponsored companies that guarantee most of the mortgages made in the U.S. To qualify for a Fannie Mae or Freddie Mac guarantee, a mortgage borrower must either make a down payment of at least 20 percent, or pay for mortgage insurance. That’s because mortgages with down payments less than 20 percent are considered more risky for the lender.

Not all mortgages are guaranteed by Fannie Mae or Freddie Mac. Low down payment mortgages are offered through other government guarantee programs, such as the Federal Housing Administration (FHA), U.S. Department of Agriculture (USDA), and Department of Veterans Affairs (VA). Those programs also require mortgage insurance or other fees. Some lenders may offer their own low-down payment mortgage programs that do not require mortgage insurance or participate in any government guarantee program. Those loans typically charge higher interest rates in order to compensate for the lack of mortgage insurance and guarantee.

No matter what kind of loan you choose, if you put down less than 20 percent, you can expect to pay more for your mortgage than if you put down at least 20 percent.

Options for putting down less than 20 percent

While making a larger down payment has benefits, it’s not uncommon to make a down payment that is less than 20 percent of the purchase price. There are a variety of different loan options that allow for a low-down payment.

Here are some common options:

A conventional loan with Private Mortgage Insurance (PMI).

“Conventional” just means that the loan is not part of a specific government program. Typically, conventional loans require PMI when you put down less than 20 percent. The most common way to pay for PMI is a monthly premium, added to your monthly mortgage payment. Most lenders offer conventional loans with PMI for down payments ranging from 5 percent to 15 percent. Some lenders may offer conventional loans with 3 percent down payments.

A Federal Housing Administration (FHA) loan.

FHA loans are available with a down payment of 3.5 percent or higher. FHA loans are often a good choice for buyers wanting to make a low-down payment. However, borrowers with higher credit scores or who can afford a somewhat higher down payment (5 to 15 percent) may find that an FHA loan is more expensive than a conventional loan with private mortgage insurance. Compare different loan options before making a decision.

Special loan programs.

Special zero down payment programs exist for veterans, service-members and rural borrowers. State and local programs may offer down payment assistance or other special loan options for low-and-moderate-income families, public service employees, and other specific populations. Depending on your situation, these programs may or may not be a better fit for you than an FHA or conventional loan. Make sure to compare the full cost of each option before making a decision.

Down Payments

Source: (CFPB) Consumer Financial Protection Bureau